Debts: High borrowing leads to lending curbs

With both public and household debts on a high, concerns are expressed if it's sustainable

AFTER Standard Chartered published its report in July noting that Singapore households had borrowings worth 151% of their annual income in 2012, making them among the most indebted in Asia, the bank warned that as interest rates rise, debt servicing may become difficult for home owners.

Housing

The Monetary Authority of Singapore (MAS) responded quickly, assuring that the local banking system was sound, while cautioning “about 5% to 10% of borrowers have a monthly debt servicing burden greater than 60% of their monthly income. It is reasonable to consider them as over-leveraged”.

Thus to mitigate risk on housing loans [housing loans make up more than 70% of household debt], MAS decided to apply the Total Debt Servicing Ratio (TDSR) framework to the granting and re-financing of property-related loans for a start. “A large property-related loan can lead to serious over-borrowing, and applying the TDSR will mitigate that risk,” noted the authority's spokesperson.

Credit card

The credit card default rate in Singapore is below 0.2% across all age groups. To ensure that it remains like this, MAS has imposed a minimum income eligibility criteria for the issue of credit cards. Individuals who are 55 years old and below must have an annual income of at least $30,000 before they can qualify for credit cards; those above 55 years of age must have an annual income of at least $15,000. In addition, MAS has a limit of up to four months’ income on the total amount of unsecured credit that can be extended to any credit card-holder.

Furthermore, the latest measures implemented on September 11 include the introduction of an industry-wide aggregate cap on individuals’ unsecured borrowings. “With this cap, financial institutions will not be allowed to grant further credit to individuals whose aggregate unsecured borrowings across all financial institutions exceed 12 months of their income for 90 days or more. This cap is designed to discourage individuals from prolonged reliance on credit cards and unsecured credit,” said the MAS.

Additionally, financial institutions will not be allowed to grant further credit to individuals whose debts with a financial institution are more than 60 days past due.

“Ultimately, while MAS has rules in place to help Singaporeans avoid accumulating excessive debt, Singaporeans have to take personal responsibility for their finances. They have to exercise prudence when deciding whether to sign up for a credit card, understand their ability to repay the debt incurred when they use the card and ensure that they do not incur excessive debt,” said Tharman recently.

“local banks are sound”

In reply to a parliamentary question on the most recent stress test conducted for banks in Singapore, Tharman Shanmugaratnam, deputy Prime Minister and in-charge of MAS said, “Earlier this year, MAS completed a stress test exercise based on end-2012 data. The results showed that the banking system as a whole remained sound, and able to withstand adverse scenarios. The local banks in particular would be able to maintain adequate financial buffers above MAS’ regulatory requirements under the prescribed stress scenarios.”

“Moody’s and Standard & Poor’s (S&P) reached similar conclusions. Moody’s found that the three local banks have enough capital to withstand even the severe stress test scenarios the agency considered. Moody’s continues to assign the local banks the highest average credit ratings (Aa1) amongst banking systems globally, but has placed this rating on a ‘negative’ outlook, i.e. to indicate the possibility of a downgrade, especially if loan defaults were to rise when interest rates go up. S&P recently affirmed the local banks strong AA- ratings and a 'stable’ outlook, based on their strong financial profiles and prudent management strategies.”

Public debt – 111.4% of GDP

According to US Central Intelligence Agency (CIA) public debt factbook, Singapore's ranks 11th in the world with its public debt 111.40% of GDP, according to 2012 estimates. The factbook adds, “For Singapore, public debt consists largely of Singapore Government Securities (SGS) issued to assist the Central Provident Fund (CPF), which administers Singapore's defined contribution pension fund; special issues of SGS (SSGS) are held by the CPF, and are non-tradable; the government has not borrowed to finance deficit expenditures since the 1980s.”

This anomaly is because of Singapore's unique system, where the government doesn't borrow to fund its budget [prevented by the constitution as well as the Government Securities Act]. To add to it, the government is required to run a balanced budget over its every five-year-term. Government debt issuances are therefore invested and not spent on the budget.

The government explains it further, “Singapore has no net debt. Its large gross debt position is due to the issuance of government securities. However, the government’s assets substantially exceed these debts. This can be seen from the fact that the government has significant net investment returns that can be spent on the budget each year. Under the constitution, the government is able to spend from the net investment returns only if it enjoys a positive net asset position. In other words, if the government’s assets fall short of its liabilities, there can be no contribution from the investment returns on reserves in the government budget. After deducting all the government’s liabilities (including CPF monies), the remaining net assets produce significant returns. The net investment returns contribution (NIRC) is about $7 billion; it should be further noted that the NIRC only comprises up to 50% of the returns earned on the reserves.”

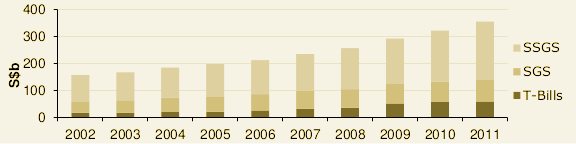

As on December 2011, total outstanding government borrowing stood at S$354 billion. Of this, SGS stock is valued at S$79 billion, the stock of Treasury-Bills is valued at S$59 billion and SSGS stock is valued at S$216 billion.

Government's borrowing over the past decade

Courtesy: Accountant-General's Department